How affordability checks work at UK casinos

TL;DR:

- Most UK casino affordability checks are quick, non-intrusive, and only assess signs of serious financial distress.

- They use soft searches that do not impact credit scores and are triggered mainly by high deposit levels crossing set thresholds.

Most UK players hear “affordability check” and immediately picture a casino demanding bank statements, payslips, and a full financial audit before they can spin a slot. That fear is understandable but largely misplaced. Understanding how do affordability checks work UK casino is far less invasive in practice than the headlines suggest. The UK Gambling Commission has been clear on this distinction, separating financial risk checks from true affordability assessments. By the end of this article, you will know exactly what triggers these checks, what casinos can and cannot ask for, and how to keep your gaming experience smooth.

Table of Contents

- Key takeaways

- How do affordability checks work at a UK casino?

- What triggers a check and what happens next

- Common concerns about casino affordability checks

- Practical tips for navigating checks smoothly

- Casino checks vs other financial checks

- My honest take on affordability checks

- Play with confidence at trusted UK casinos

- FAQ

Key takeaways

| Point | Details |

|---|---|

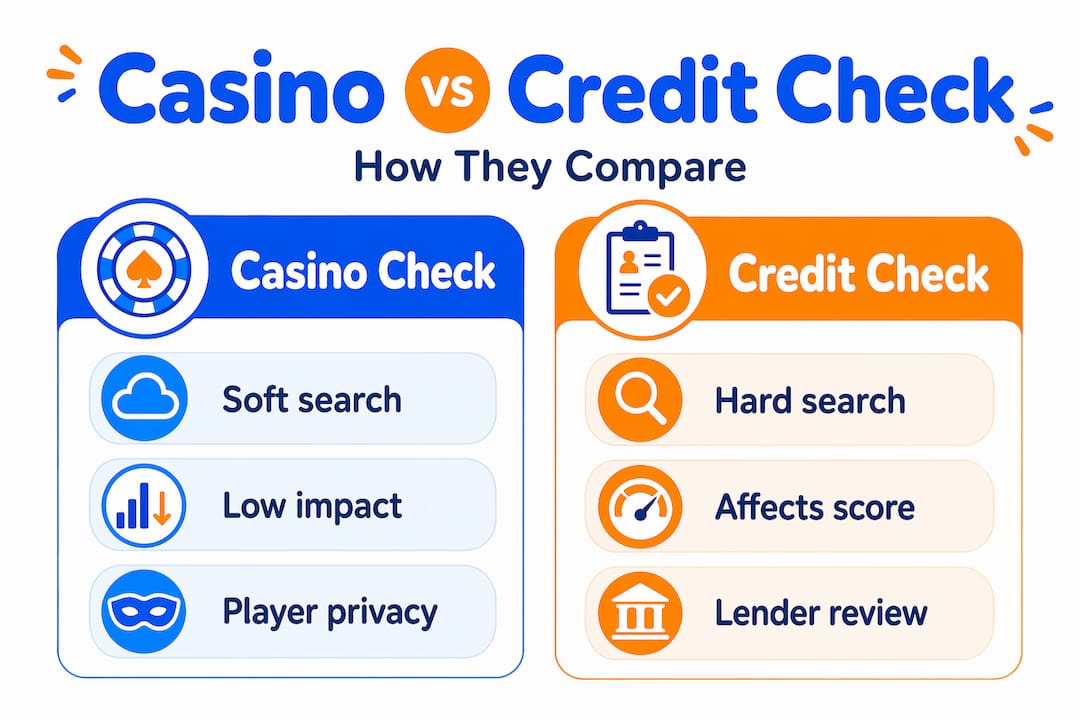

| Checks are not credit checks | Affordability checks use soft searches only, leaving zero impact on your credit score. |

| Most checks are frictionless | Around 97% of financial risk checks complete automatically without players noticing anything. |

| Document requests are discouraged | The Gambling Commission actively discourages casinos from asking for bank statements or payslips. |

| Checks target financial distress | These checks flag serious issues like bankruptcy, not everyday spending habits. |

| Triggers vary by deposit level | Most checks are activated when monthly deposits cross a set spending threshold. |

How do affordability checks work at a UK casino?

Affordability checks UK casinos perform are, at their core, financial risk assessments. They are not a judgement on whether you can “afford” to gamble in a lifestyle sense. The Gambling Commission introduced them to identify players who show genuine signs of financial distress, such as active debt management plans, county court judgements, or bankruptcy proceedings.

This distinction matters enormously. A financial risk check is designed to protect someone who is gambling while insolvent, not to police what a financially stable person chooses to spend on entertainment. The regulator has been explicit that these checks should not replicate the affordability assessments used in consumer lending.

Here is what the process is actually looking for:

- Signs of active insolvency or bankruptcy

- County court judgements (CCJs) or individual voluntary arrangements (IVAs)

- Accounts flagged in debt management with credit reference agencies

- Indicators of significant arrears across financial products

- Patterns that, taken together, suggest acute financial vulnerability

The data behind these checks comes from the same credit reference agencies, Experian, Equifax, and TransUnion, that lenders use. But the criteria applied are very different from a mortgage assessment. Casinos are not looking at your credit score or your disposable income. They are looking for red flags that signal someone is already in serious trouble.

What triggers a check and what happens next

Understanding how UK casino checks work in practice means knowing when they kick in and what the process looks like from your side of the screen.

Step 1: Spending thresholds. Most UK-licensed casinos set a monthly deposit threshold after which a financial risk assessment is triggered. The precise figures vary between operators, but they typically run into the hundreds of pounds within a rolling 30-day window.

Step 2: Automated data request. Once a threshold is crossed, the casino’s system sends an automated query to a credit reference agency. This soft credit search returns financial risk markers without triggering a hard footprint on your credit file.

Step 3: Automated outcome. In the vast majority of cases, the check completes instantly. The 97% frictionless completion rate achieved in the UKGC pilot demonstrates this well. You keep playing and never notice anything has happened.

Step 4: Flag raised for a small minority. If the data returns a risk flag, affecting roughly 3% of accounts in the pilot, the casino may pause further deposits or contact you for more context. These flagged players showed two to five times the likelihood of financial difficulties compared to the general player base.

Step 5: Enhanced review. Only about 0.1% of accounts, one in every thousand, require any form of follow-up contact or additional support. Even then, the Gambling Commission’s guidance makes clear that casinos should not be requesting bank statements or payslips at this stage.

Pro Tip: Check your own credit file through a soft search via Experian, Equifax, or TransUnion before depositing heavily at a casino. You will see exactly what they see, and you can address any errors before they cause unwanted friction.

Common concerns about casino affordability checks

Fears around affordability assessments in UK gambling cluster around a few recurring themes. Here is an honest look at the most common ones.

- “Will the casino see my bank statements?” The Gambling Commission has actively moved to prevent operators from requesting excessive financial documents. Standard financial risk checks do not involve statements, and the regulator considers asking for them to be outside the legitimate scope of the process.

- “Will this hurt my credit score?” No. These are soft searches with zero credit score impact, invisible to other lenders and completely harmless to mortgage or loan applications.

- “Could I be refused for having a low income?” Income level alone is not assessed. The checks look for distress indicators, not salary brackets.

- “Will I have to prove my earnings?” Only in rare and specific circumstances involving very high spend levels and genuine risk flags. Even then, the regulator expects proportionate and non-intrusive requests.

The industry itself is not without concerns, though. The Betting and Gaming Council has raised worries that perceived friction from these checks may push high-spending players towards unlicensed black-market operators who carry none of the consumer protections a licensed UK site provides. That is a legitimate tension the regulator is still working through.

“Financial risk checks in gambling are designed more to protect players in real distress than to monitor everyday spending.” — UK Gambling Commission guidance via iGaming.org

The Gambling Commission’s position is that transparency in how checks are applied is the key to maintaining player trust. Operators who communicate clearly about what triggers a check and what it involves will face far less resistance from their players.

Practical tips for navigating checks smoothly

Understanding UK gambling affordability issues is one thing. Knowing how to keep your experience friction-free is another. Here is what actually works.

Keep your credit file accurate. Errors on your credit report are more common than people realise. A dormant account incorrectly marked as defaulted, for instance, could trigger a risk flag. The UK’s multiple credit agencies each hold slightly different data, so check all three if you want a complete picture.

Know your thresholds. Different casinos set different trigger points. Reading the responsible gambling section of any casino you use regularly will often give you a sense of where their monitoring kicks in. Some operators are transparent about this in their terms.

Respond promptly if contacted. If your casino does reach out with a question about your activity, a prompt and honest response resolves the matter far faster than ignoring it. Delays in responding typically result in deposit restrictions while the casino waits.

Pro Tip: Large withdrawal requests tend to process more slowly when submitted on Friday afternoons or over the weekend. Compliance teams are smaller outside business hours and manual reviews can push payouts into the following week. Submit big withdrawals on weekday mornings for the fastest handling.

- Review your Experian, Equifax, and TransUnion reports at least twice a year

- Avoid applying for multiple credit products in the weeks before large casino deposits, as this can create unnecessary noise in your file

- Use a secure, regulated casino that clearly states its responsible gambling and financial check processes upfront

Casino checks vs other financial checks

This is where the confusion between affordability checks and real credit checks often runs deepest. They share some infrastructure but serve very different purposes.

| Feature | Casino financial risk check | Lender credit assessment |

|---|---|---|

| Type of search | Soft only | Hard search (usually) |

| Credit score impact | None | Can reduce score temporarily |

| Data reviewed | Risk flags only (CCJs, IVAs, bankruptcy) | Full credit history, income, outgoings |

| Decision output | Continue, flag, or pause account | Approve, decline, or counter-offer loan |

| Visible to other lenders | No | Yes |

| Assesses income level | No | Yes |

| Regulated by | UK Gambling Commission | Financial Conduct Authority |

Lenders assess your full credit report: payment history, credit utilisation, electoral roll status, and often income verification. A casino’s financial risk assessment is a narrower instrument. It asks one question: does this person show signs of serious financial distress? It does not ask whether you have a good credit score or whether you are financially prudent.

Soft searches appear on your own credit file when you check it, but they are invisible to any third party. Hard searches, like those from a mortgage application, are visible to other lenders for up to two years. Casino checks never leave that kind of footprint.

The casino security processes at well-run UK operators are built around this soft-search model specifically to minimise any unintended consequences for players.

My honest take on affordability checks

I have watched the debate around affordability checks play out for a couple of years now, and the dominant narrative still frustrates me. Too many players assume the worst, and too many critics frame these checks as government overreach into personal finances.

In my experience, the practical reality is much quieter. The vast majority of players never interact with these checks at all because frictionless completion is the norm, not the exception. The people who do get flagged are, statistically, in genuine difficulty. That matters. A casino continuing to take deposits from someone in active bankruptcy proceedings is not a neutral act.

Where I think the industry falls short is in communication. Casinos are often too secretive about how these checks work, which breeds exactly the kind of suspicion that makes players nervous. If operators were upfront from the start, spelling out what triggers a check and what will never be asked for, a lot of the anxiety would dissolve. Until that cultural shift happens more broadly, knowing the rules yourself is your best protection.

The players who struggle most with these checks are those who have errors on their credit files that they are unaware of, not those with high incomes or big deposits. That is a solvable problem, and it starts with checking your own data.

— Traffic

Play with confidence at trusted UK casinos

Knowing how casino checks work is half the battle. The other half is choosing operators who handle them properly. Licensed UK casinos that follow Gambling Commission guidance conduct these checks without drama, without demanding your payslips, and without disrupting your play. At Geekygambler, every casino in our directory has been assessed for regulatory compliance, including how operators manage financial risk processes. Browse our UK casino reviews to find operators with verified licences, transparent terms, and responsible gambling tools that actually work. If you want to go deeper on what makes a casino genuinely safe to use, our secure casino guide is a good next step.

FAQ

Do affordability checks affect my credit score?

No. Casino affordability checks use soft searches only, which have zero impact on your credit score and are invisible to other lenders. They will not affect mortgage, loan, or any other credit applications.

Can a casino ask for my bank statements?

The Gambling Commission actively discourages casinos from requesting bank statements or payslips as part of financial risk checks, and considers such requests outside the legitimate scope of the process.

How many players are actually flagged by these checks?

Only around 3% of players are flagged during a financial risk assessment, and just 0.1% require any follow-up contact. The vast majority of checks complete automatically without the player noticing.

What triggers an affordability check at a UK casino?

Checks are typically triggered when a player’s deposits cross a set monthly threshold. The exact figure varies by operator, but once the threshold is crossed, an automated soft search is performed against credit reference agency data.

Are these checks the same as a credit check from a bank?

No. A bank credit check is a hard search that reviews your full financial history and can affect your credit score. A casino financial risk check is a soft search that looks only for serious distress indicators such as bankruptcy or county court judgements, and leaves no trace on your credit file.