UKGC affordability check threshold 2026 explained

TL;DR:

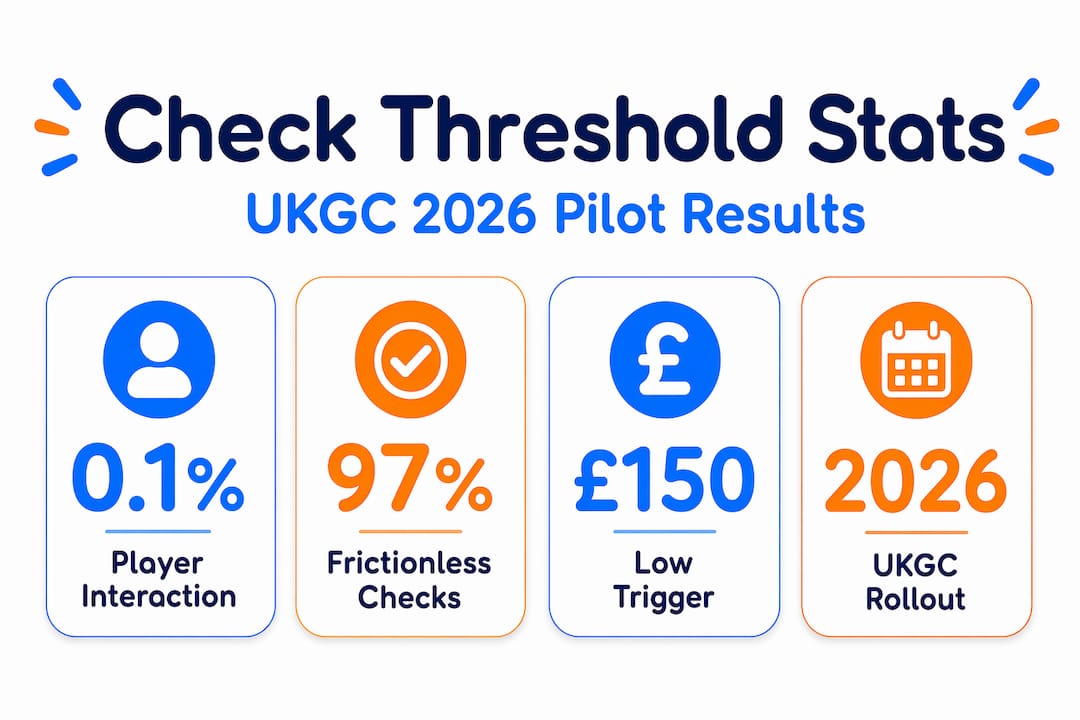

- The UKGC affordability check threshold in 2026 is set at £150 in net deposits over a rolling 30-day period, triggering mostly invisible, soft-credit checks. Most players will experience no disruption, as only a small percentage are subject to deeper assessments at higher loss levels, without affecting credit scores or routine document requests. Understanding this system helps players manage their deposits responsibly and avoid unnecessary concern amid media coverage and regulatory updates.

If you’ve heard that the UKGC affordability check threshold 2026 means casinos will demand your payslips before you can place a bet, you’ve been misled. The reality is far narrower. Since February 2025, operators must run light-touch financial checks when a player reaches £150 in net deposits over a rolling 30-day period. Most players will never notice these checks at all. This guide breaks down exactly how the threshold works, what triggers a deeper assessment, and what it all means for your experience as a UK gambler trying to play safely and responsibly.

Table of Contents

- Key takeaways

- Regulatory background and context

- The £150 threshold: what it means in practice

- What actually happens during a check

- Addressing fears and misconceptions

- How to prepare as a UK player

- My take on the 2026 threshold

- Find UKGC-compliant casinos you can trust

- FAQ

Key takeaways

| Point | Details |

|---|---|

| £150 net deposit trigger | Light-touch checks begin when net deposits hit £150 in any rolling 30-day window. |

| Checks are mostly invisible | 97% of assessments in the pilot were frictionless, meaning most players experienced nothing at all. |

| No credit score impact | Soft credit reference data is used; it does not appear on your credit file or affect lending decisions. |

| Enhanced checks have higher bars | A separate, deeper assessment kicks in only at £1,000 net loss in 24 hours or £2,000 over 90 days. |

| Documents rarely requested | Bank statements and payslips are not a routine part of these checks. |

Regulatory background and context

To understand the UKGC affordability check threshold 2026, you first need to understand where it came from and what problem it is trying to solve. The UK Gambling Commission has been building towards financial risk assessments for several years. The goal was never to police how much people spend on gambling. It was to identify the small proportion of players showing early signs of financial distress before significant harm sets in.

The UKGC ran a formal pilot programme for financial risk assessments before any widespread rollout. That pilot produced some striking results. 97% of checks were frictionless, exceeding the UKGC’s own 80% target. This was not a system designed to interrogate ordinary players. It was designed to work quietly in the background for the vast majority.

It helps to distinguish between two types of checks that often get muddled in news coverage. An affordability check is a broad concept, sometimes used loosely to describe any operator review of a customer’s financial situation. A financial risk assessment is the specific mechanism the UKGC developed. It relies primarily on background credit data rather than income disclosure from the player directly.

This matters because the two terms carry very different implications. One sounds like a bank interview. The other is closer to a background process you would never know was running. The UKGC’s 2026 regulatory environment also sits alongside changes like increased Remote Gaming Duty and tighter stake limits, creating a layered compliance picture for operators.

Pro Tip: When reading headlines about affordability checks, check whether the article is discussing financial risk assessments specifically or using the term loosely. The distinction changes the story significantly.

Key points worth holding onto from this regulatory background:

- The UKGC’s pilot focused on identifying markers of financial harm, not measuring overall disposable income

- Financial risk assessments use soft credit reference signals, not hard credit searches

- The checks are targeted at the top 3% of high-spending accounts, not the general gambling population

- Regulatory goals are to support vulnerable players while minimising friction for everyone else

The £150 threshold: what it means in practice

Here is the specific mechanics of the UKGC affordability check threshold 2026. The trigger point is £150 in net deposits over a rolling 30-day period. Net deposits means your total deposits minus your total withdrawals within that window. So if you deposit £200 but withdraw £100, your net deposit figure is £100, which sits below the threshold.

This is worth understanding precisely because it changes how the threshold actually affects behaviour. A player who deposits and withdraws regularly, moving money back and forth, may take considerably longer to cross £150 net than a player who only deposits. The calculation rewards players who cash out winnings rather than leaving funds on site.

Here is how the process typically unfolds:

- You reach £150 in net deposits across any rolling 30-day window at a UKGC-licensed operator

- The operator runs a light-touch financial risk assessment using soft credit reference data

- In most cases, the check completes in the background and you notice nothing

- If the credit data suggests no financial vulnerability, your experience continues unchanged

- If markers of concern are identified, the operator may take proportionate action

The threshold for this light-touch check is deliberately set low to catch early warning signs. The design philosophy is early intervention rather than waiting for a player to rack up serious losses. This is distinct from the enhanced checks triggered at £1,000 in net losses over 24 hours or £2,000 over 90 days, which represent a significantly higher level of scrutiny.

The UKGC was precise in pilot data: only 0.1% of accounts actually triggered a check requiring any player interaction at all. That is lower than the 0.6% originally projected. Put another way, for every 1,000 players, roughly one would ever be asked to do anything. Everyone else would simply continue playing.

Understanding your responsible gambling rights as a UK player helps you approach these assessments from a position of knowledge rather than anxiety.

What actually happens during a check

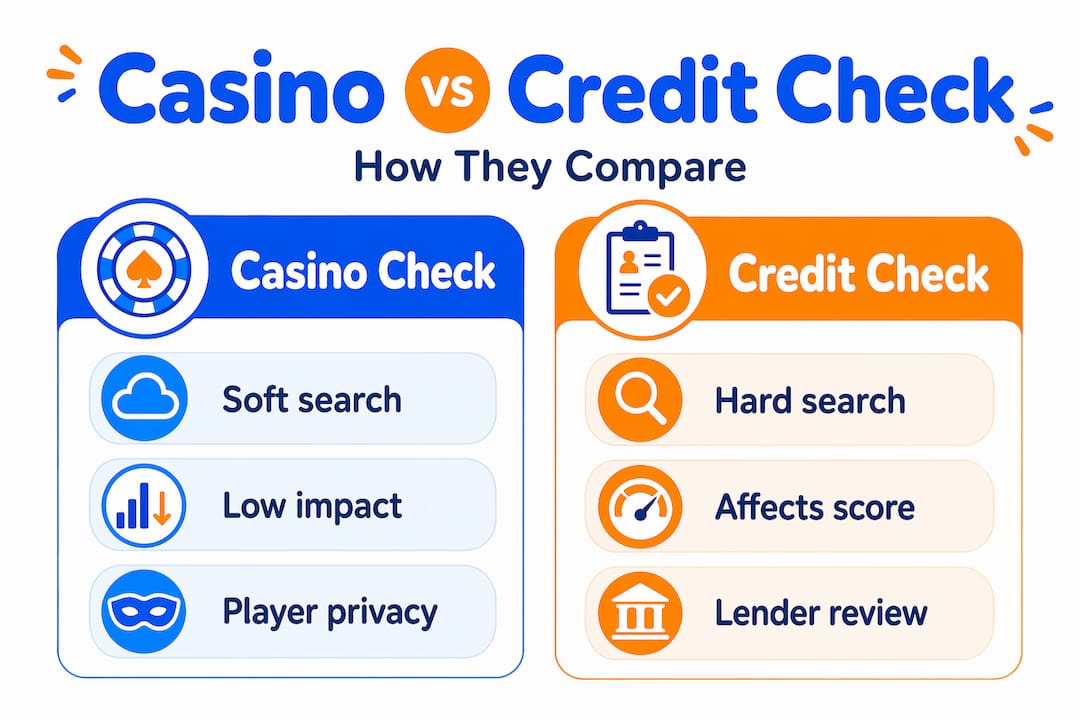

The mechanics of how a financial risk assessment runs will reassure most readers. The operator does not call you. It does not send a form. What happens is that the operator queries credit reference data using a soft search. Soft credit searches are completely invisible to lenders. They do not affect your credit score. They do not show up on your credit report in the way a mortgage application or credit card search would.

The data being reviewed looks for specific markers of financial vulnerability, such as indicators of recent County Court Judgments, debt management plans, or other signals that a person may be under financial strain. The regulator focuses on markers of financial harm rather than a blunt income assessment.

What this means for you:

- You will not receive a notification in most cases

- Your casino session will continue normally if no concern is flagged

- Document requests are not routine; bank statements and payslips are an exception, not the rule

- Operators are required to act proportionately if vulnerability is identified, which might mean deposit limit suggestions or changes to marketing communications rather than an outright ban

Pro Tip: If an operator does contact you requesting documents, that is a sign you have potentially crossed into the enhanced check territory. Ask them specifically which threshold has triggered the request.

The enhanced check tier, triggered at those higher net loss figures, does involve more detailed assessment. But even then, operators are expected to act proportionately rather than automatically restricting accounts. The goal is sustainable gambling support, not reflexive account closures. This is an important distinction that much of the media coverage around affordability checks has failed to make clearly.

Addressing fears and misconceptions

A lot of anxiety has built up around these checks, and much of it is based on inaccurate interpretations. Here are the most common fears and what the evidence actually says.

“Affordability checks will let casinos decide what I can and cannot spend.”

This misunderstands the regulatory intent. The checks are not a spending cap. They are a vulnerability signal. If you show no markers of financial distress, the check has no practical effect on your gameplay whatsoever. The UKGC’s own language focuses on identifying harm, not managing budgets.

Compare the common fears against the actual reality:

| Common fear | Actual position |

|---|---|

| Checks will hurt my credit score | Soft searches are invisible to lenders and credit reference files |

| I will have to submit payslips and bank statements | Document checks are not required for standard financial risk assessments |

| Most gamblers will be affected | Only the top 3% of high-spending accounts are targeted; 0.1% see any friction |

| Checks will lead to account closures | Operators must act proportionately; restrictions are graduated, not automatic |

| Players will move to unregulated sites | Fears about migration to black-market operators are unsubstantiated at pilot stage |

The evidence from the pilot is genuinely reassuring. The system processed a large volume of assessments, with the vast majority completing without any player interaction at all. The UKGC’s regulatory approach in 2026 continues to be grounded in proportionality rather than restriction for its own sake.

How to prepare as a UK player

Being an informed player is the most effective thing you can do. Here is practical guidance on living with the 2026 affordability check framework.

Track your net deposits, not just your deposits. Most players focus on how much they deposit. But the trigger uses net deposits, so withdrawing winnings regularly reduces your net figure and pushes the threshold further away.

Practical steps worth taking:

- Review your deposit and withdrawal history monthly to understand your net position across your active accounts

- Use deposit limit tools that most UKGC-regulated casinos now offer as standard; these sit neatly alongside the new responsible gambling tools available to UK players

- If you receive a communication from an operator about a financial assessment, respond calmly; ask which threshold was triggered before providing anything

- Understand that requests for documents at the light-touch stage are unusual and you are entitled to query them

- If you are genuinely concerned about your gambling habits rather than the regulatory process, organisations like GamCare provide free, confidential support

For players who gamble at multiple sites, the threshold applies per operator, not across the industry as a whole. There is no central database pooling net deposit figures across all your casino accounts. Each operator runs its own assessment independently.

Staying informed about UK online casino regulations in 2026 helps you make better decisions about which platforms to use and how to manage your activity sensibly.

My take on the 2026 threshold

I will be direct about this. Most of the fear around the UKGC affordability check threshold 2026 is disproportionate to what the system actually does. I have followed this regulatory debate closely, and what strikes me most is the gap between how checks are reported and what the data shows.

The pilot results tell a clear story. 97% frictionless is not a system that is going to disrupt the average player’s evening. It is a system designed to catch a very small group of people before they reach a crisis. That is a goal most people would support if they thought about it clearly rather than reacting to worst-case headlines.

What concerns me more is the cumulative regulatory burden on operators in 2026. Remote Gaming Duty increases, stake limits, and affordability checks all arriving in the same period creates compliance pressure that could affect smaller operators disproportionately. That has real consequences for the variety of sites available to UK players.

My practical advice is this: understand the threshold, track your net deposits, and do not panic if you are contacted. The system is narrower and less intrusive than the headlines suggest.

— Traffic

Find UKGC-compliant casinos you can trust

Knowing the rules is half the picture. The other half is playing at sites that take their obligations seriously.

At Geekygambler, every casino in our listings is independently reviewed for UKGC compliance, including how operators handle financial risk assessments and responsible gambling tools. Our expert casino reviews assess each site’s transparency, fairness, and player protections. If you want to find a platform that handles affordability checks properly without making your experience more complicated than it needs to be, our reviews give you the verified information to choose with confidence.

FAQ

What is the UKGC affordability check threshold in 2026?

The threshold is £150 in net deposits over a rolling 30-day period. When a player crosses this figure at a UKGC-licensed operator, a light-touch financial risk assessment is triggered automatically in the background.

Will an affordability check affect my credit score?

No. The checks use soft credit reference searches that are completely invisible to lenders and do not appear on your credit report in any way that would affect borrowing decisions.

Do I need to provide bank statements or payslips?

Document checks are not a routine part of the standard light-touch assessment. Most players will never be asked to provide any paperwork at all.

What triggers an enhanced affordability check?

Enhanced checks are triggered at £1,000 in net losses within 24 hours or £2,000 in net losses over a 90-day period. These involve a more detailed assessment than the standard light-touch check.

Does the £150 threshold apply across all my casino accounts combined?

No. Each UKGC-licensed operator runs assessments independently. The threshold applies separately at each site and is not pooled across multiple operators or a central industry database.